Stefán Ólafsson writes.

There has been a great deal of discussion about how wages for the general public have risen significantly in recent periods. The Confederation of Icelandic Employers (SA) regularly brings this up, and the Central Bank does as well.

However, in all this constant emphasis on wage increases for ordinary workers, little attention is generally paid to the development of capital income or property income. These are the earnings that wealthier individuals receive from income-generating assets such as shares, bonds, real estate, savings, and private businesses.

In general, the wealthiest people in society receive the largest share of their income in the form of capital income. For example, the top ten percent of earners received around 70% of all capital income in recent years. The top one percent receives the majority of its income as capital income. In other words, substantial capital income flows primarily to the richest members of society.

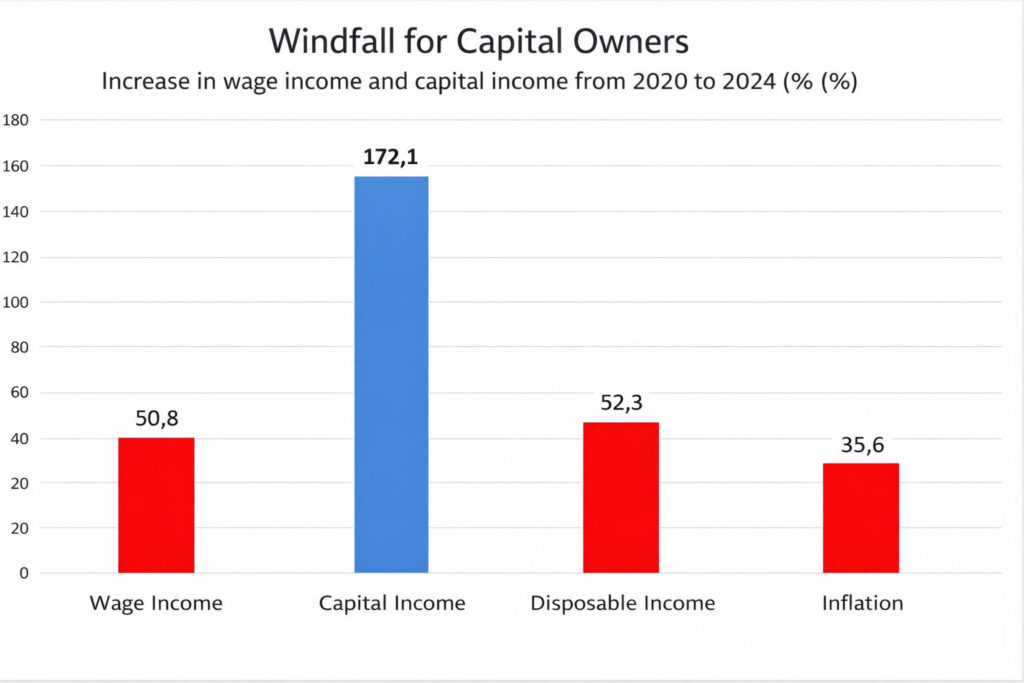

Let us look at how these incomes have grown compared to the wage income of the general public over the period from 2020 to 2024. The data come from Statistics Iceland.

As the chart shows, property income/capital income increased by 172% during this period, while wage income rose by 50.8%. Capital income has therefore increased more than three times as much as wage income. For comparison, cumulative inflation over the period (35.6%) and the increase in household disposable income (52.3%) are also shown.

This reflects a major windfall for the wealthy. Companies have generated strong returns, and investments in securities likewise. Wealthy investors who in recent years have purchased large numbers of new apartments on the housing market, sometimes entire buildings, to rent out to tourists or others have made substantial profits from the housing crisis, which is eroding the purchasing power of ordinary workers and tenants. Those who have been able to save large amounts in bank accounts have also benefited from the Central Bank’s high interest rate environment. Their interest income has grown the fastest among the components of capital income.

The role of capital income in inflation

Perhaps the Central Bank should focus on this group, which has the highest incomes in society and sustains high levels of consumption and investment that drive demand-pull inflation. It is not low-wage workers or indebted young people who are the main drivers of inflation. The Bank’s high interest rate policy, however, impacts lower-income and indebted groups the most, while sparing higher-income and wealthier individuals. This is poor and unjust economic management, and it also fails to deliver sufficient results in the fight against inflation.

In the United States, the top ten percent of earners account for around half of total private consumption. A similar pattern is seen in Iceland. If it is necessary to reduce private consumption to curb inflation, the most direct approach is to reduce the consumption of higher-income and wealthier groups, for example, through higher taxes on capital income and top wages.

Finally, it should also be noted that those with substantial capital income benefit from significant tax advantages, as capital income is taxed at lower rates than wage income. They do not even pay municipal taxes on this income.

In the past, it was considered appropriate that people who worked hard and secured housing for their families should receive tax benefits, for example, in the form of interest rebates. That is no longer the case. Today, the greatest tax advantages go to capital owners who let their money work for them. Such an arrangement undermines work ethics and encourages unproductive speculation.

The windfall for capital owners since 2020 is due both to the large increase in capital income and to the substantial tax advantages it enjoys. Above all, however, this kind of state generosity toward the wealthiest, in the form of lower taxation of capital income than wage income, is both unnecessary and unjust. In fact, it is harmful, as it contributes to inflation.

Stefán Ólafsson is an expert at Efling Union and a professor emeritus at HÍ.